Energy and Logistics Shock Spreading to the Seafood Market

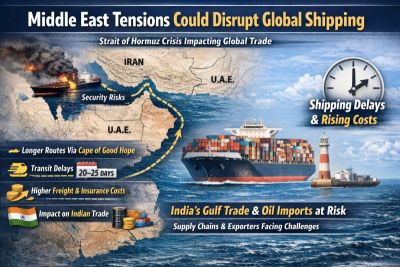

Recent developments in the Middle East are creating a significant cost shock for global trade. One of the key hotspots is the Strait of Hormuz – a critical global shipping lane through which around 20% of the world’s traded oil passes.

In early March 2026, Brent crude oil prices briefly surged to nearly USD 120 per barrel before easing to around USD 92 per barrel by March 10, 2026. At the same time, war risk insurance premiums for commercial vessels operating in the Middle East have risen sharply.

Shipping data shows that vessel traffic through the Strait of Hormuz has declined noticeably in a short period due to security risks. Many shipping lines have adjusted routes or introduced additional risk surcharges. Container freight costs have also begun to rise again. The global container freight index increased by 3% on March 5, 2026, reaching USD 1,958 per 40-foot container.

Air freight — an important channel for fresh seafood — has also been significantly affected. According to estimates from international logistics analysts, the conflict has reduced global air cargo capacity by around 12%.

For the seafood industry, this development is particularly important. Logistics costs already account for a significant portion of export prices, especially for frozen products or items requiring rapid transportation such as fresh tuna. As fuel and insurance costs rise, expenses for refrigerated container shipping, air freight, and cold-chain storage inevitably increase.

The U.S. Market Remains Highly Dependent on Imports

The United States is currently the world’s largest seafood consumption market and relies heavily on imported supply. It is estimated that about 80% of seafood consumed in the U.S. is imported, while per-capita consumption exceeds 19 pounds per year. Total annual U.S. imports of edible seafood reach approximately 6.3 billion pounds.

This high level of import dependence makes U.S. seafood demand particularly sensitive to external cost shocks.

Retail data from early 2026 shows an interesting trend: seafood prices are rising faster than consumption volumes. In January 2026:

-

Frozen seafood sales increased by 4.5% to USD 860.7 million, while volume declined 3.8%

-

Fresh seafood sales rose 3.7% to USD 856.6 million, while consumption volumes remained nearly flat

This trend suggests that American consumers are still spending on seafood but are becoming increasingly sensitive to price changes.

Shrimp: The Most Price-Sensitive Product

Among the major seafood categories in the U.S. market, shrimp shows the clearest sensitivity to price fluctuations.

Retail data for January 2026 shows:

-

Fresh shrimp: price up 17.3%, volume down 18.4%

-

Frozen shrimp: price up 16%, volume down 10.7%

These figures indicate that when retail prices rise significantly, American consumers tend to reduce shrimp purchases more quickly than many other seafood products.

In 2025, the United States imported about 795,641 tons of shrimp, up 2% compared to the previous year. However, if transportation costs continue to rise and are passed on to retail prices, shrimp demand — particularly for premium products — could face the strongest pressure.

Affordable Seafood May Gain More Attention

During periods of economic uncertainty, consumers often shift toward more affordable food options. This trend could create opportunities for certain seafood categories.

In 2025:

-

The U.S. imported 91.9 million pounds of frozen Yellowfin tuna

-

Global exports of frozen surimi blocks reached about 145,000 tons

Products such as canned tuna, surimi, Pangasius, and other whitefish tend to maintain more stable demand during economic downturns. If living costs in the United States continue to rise, demand may gradually shift from premium seafood products to more affordable alternatives.

Retail Channels May Benefit

Another important factor is the difference between consumption channels. Restaurants and food service are typically more sensitive to economic fluctuations. When living costs increase, consumers tend to reduce dining out.

According to the U.S. Bureau of Labor Statistics, in January 2026:

-

Food away from home prices increased 4.0%

-

Food at home prices rose 2.1%

This indicates that dining out costs are rising faster than cooking at home. If this trend continues, seafood demand in restaurants may decline, while retail and at-home consumption could remain relatively stable.

Vietnam’s Seafood Exports to the U.S.

Vietnam’s seafood exports to the United States in the first two months of 2026 reached USD 209 million, down slightly 3% compared to the same period in 2025.

-

Shrimp remained the largest category with nearly USD 60 million, accounting for 28.7%, although exports dropped 22% due to the impact of anti-dumping duties

-

Tuna exports exceeded USD 42 million, down 15.1%, partly affected by regulations under the Marine Mammal Protection Act

-

Pangasius exports reached approximately USD 37.9 million, decreasing 5.3%