The global container shipping market entered June 2026 with increasingly clear signs of overheating, as freight rates surged across major trade lanes, the peak shipping season arrived earlier than usual, and effective vessel capacity continued to tighten due to geopolitical tensions, port congestion, and carrier network adjustments. Recent developments indicate that the freight rate upcycle is returning, while service quality has yet to improve accordingly.

According to Drewry’s World Container Index (WCI), global container freight rates increased by 23% during the first week of June alone, reaching USD 3,433/FEU, marking the strongest weekly increase since the beginning of the year. The primary drivers came from Asia–Europe and Trans-Pacific routes. Freight rates from Shanghai to Los Angeles rose by 31% to USD 4,565/FEU, while rates from Shanghai to Rotterdam climbed 25% to USD 3,579/FEU. At the same time, the Shanghai Containerized Freight Index (SCFI) recorded five consecutive weeks of gains, reflecting a strong market recovery trend.

Industry experts believe that this year’s peak shipping season has started earlier than normal. Early purchasing activities by retailers, congestion at several major ports, and carriers’ capacity management strategies have significantly accelerated shipping demand since late May. Major shipping lines such as CMA CGM, MSC, Maersk, and Hapag-Lloyd have continuously introduced Peak Season Surcharges (PSS) on Asia–Europe and Trans-Pacific routes to capitalize on market momentum.

Another noteworthy factor is the tightening of effective vessel supply, despite global fleet capacity remaining at historically high levels. According to Alphaliner, the idle fleet currently accounts for only approximately 0.6% of total global container shipping capacity, one of the lowest levels recorded in recent years. The repositioning of vessels toward more profitable trade lanes, combined with blank sailings and schedule adjustments, has reduced actual shipping capacity considerably below nominal fleet figures.

While freight rates continue to climb sharply, service reliability in ocean shipping has shown signs of deterioration. Analysis from data platform Xeneta highlights a recurring paradox in the container shipping industry: the higher freight rates rise, the lower schedule reliability tends to become. During the Covid-19 crisis, when freight rates exceeded USD 7,000/FEU in 2021, schedule reliability dropped to approximately 20%. A similar trend appears to be re-emerging in 2026, as congestion intensifies at major European ports such as Hamburg, Rotterdam, and Antwerp, leading to longer waiting times and increased schedule disruption risks across major trade lanes.

Although Sea-Intelligence data indicates that global schedule reliability improved to around 62.2% in March 2026, average delays still remained at 5.48 days. This suggests that the global logistics network remains highly vulnerable to new geopolitical shocks or supply chain disruptions.

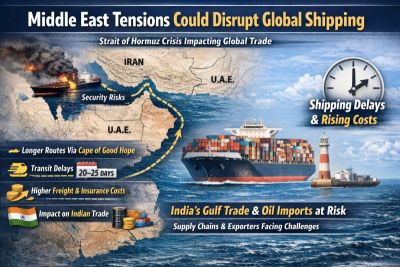

Geopolitical risks continue to dominate the ocean freight market outlook. Tensions in the Middle East, particularly surrounding the Red Sea and the Strait of Hormuz, have led many shipping lines to maintain rerouting strategies via the Cape of Good Hope instead of transiting through the Suez Canal. Longer transit routes increase fuel consumption, extend delivery times, and reduce fleet rotation efficiency. Consequently, freight costs continue to face upward pressure while effective market capacity remains constrained.

Fuel prices are also an important variable in June. Costs related to bunker fuel, aviation fuel, and inland transportation continue to be influenced by global oil price volatility. Therefore, even if base freight rates do not increase substantially, total logistics costs may still rise through fuel surcharges, emergency fees, and inland transportation expenses.

For import-export businesses, particularly in the seafood industry, the current environment suggests that transportation service selection should no longer be based solely on the lowest freight rate. Reliability, space availability, minimized transshipment risks, and total logistics cost control are becoming increasingly critical factors. Industry experts recommend that businesses secure bookings early, develop alternative shipping plans, and closely monitor freight market developments in the coming weeks, as many analysts still forecast elevated freight rates throughout the peak shipping season of Q3 2026.