According to industry reports, the Middle East’s processed and canned tuna market reached around 328,000 tons in 2024, equivalent to a value of approximately USD 1.3 billion. The region remains a net importer, with Saudi Arabia, the UAE, and Israel leading in import value.

However, 2025 has witnessed major shocks on the import side, as tuna imports in most key markets across the region have dropped sharply.

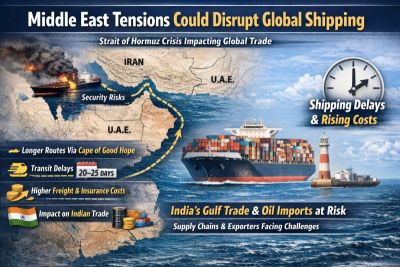

According to Vietnam Customs data, Vietnam’s tuna exports to this region in the first eight months of 2025 fell by 23% compared to the same period in 2024, reaching nearly USD 60 million. Exports to Israel declined by 48%, Lebanon by 9%, Jordan by 37%, and Saudi Arabia by 63%. These disruptions have been driven by regional conflicts and rising transportation costs, especially as the Red Sea route remains unstable.

On the positive side, exports to some markets have shown signs of recovery, such as Egypt (up 141%) and the UAE (up 16%).

Drivers & Challenges: From Logistics to Standards

One bright spot in the Middle East tuna market outlook is the steady demand for packaged tuna products—both canned and pouch formats—which are forecast to grow consistently. Reports indicate that the Middle East & Africa region could achieve even higher revenues by 2030.

Within the GCC (Gulf Cooperation Council), the tuna market was estimated at around USD 862.6 million in 2024. However, growth is expected to slow in the coming years as countries shift from purely importing to investing in domestic processing facilities to strengthen their local supply chains.

Nevertheless, logistics costs—especially reefer container rates, marine insurance through the Red Sea, and energy expenses—remain significant challenges. Exporters must invest more in cold chain systems, transshipment hubs, and traceability solutions.

In addition, Halal compliance has become increasingly common, alongside growing demands for sustainability certifications, both of which raise operational costs and require stricter quality management.

Outlook 2025 and Beyond: Growth, But at a Slower Pace

In 2025, demand for processed tuna in the Middle East is expected to remain strong—especially in the canned and pouch segments. Vietnam has opportunities to expand its market share by boosting exports to Egypt and Saudi Arabia—two strategic markets—while maintaining a stable position in the UAE and Israel.

Globally, the tuna import market is projected to reach 1.75–1.8 million tons in 2025, with a total value exceeding USD 9 billion. Within the Middle East, forecasts for 2025–2030 suggest modest growth, as the packaged tuna market in the Middle East & Africa continues to expand, albeit at a slower rate.

By 2035, the Middle East’s processed tuna market is expected to reach approximately 366,000 tons, worth around USD 1.6 billion. Most growth potential will come from Gulf countries, where investments in infrastructure, strategic imports, and local processing development are being prioritized.

Key risks for exporters include the ongoing instability in the Red Sea, which drives up freight costs and delivery times, and the potential for wider trade disruptions if regional conflicts escalate further.

Conclusion

2025 is a challenging year for the Middle East tuna market: demand remains strong, yet import disruptions and rising costs continue to squeeze profit margins. In the long term, the market is expected to grow steadily but slowly.

With logistics infrastructure, cold chain efficiency, and compliance with Halal, traceability, and sustainability standards becoming decisive factors, exporters with flexible strategies and strong risk management will hold a clear advantage in this highly competitive market.